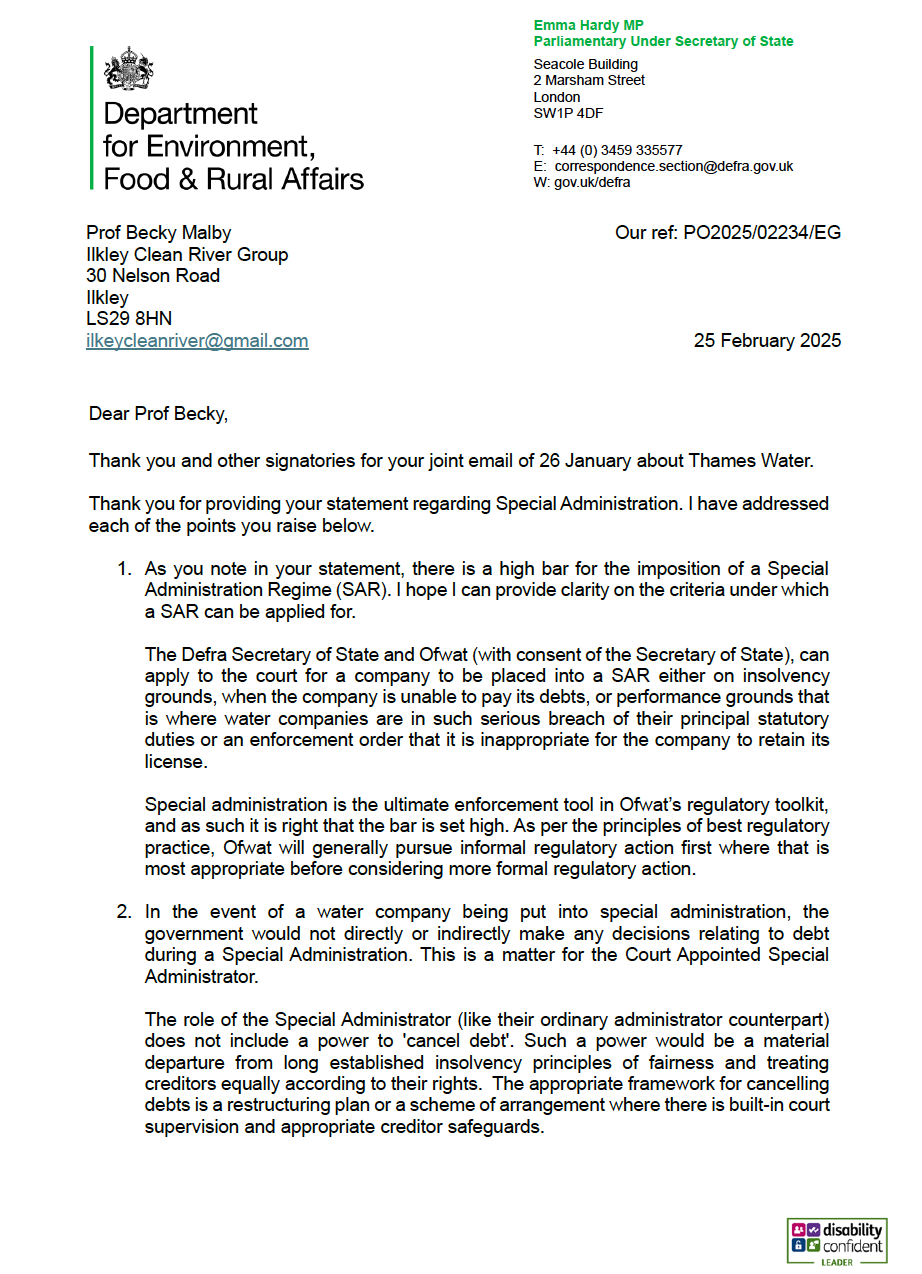

Our Response

- Apply to the court to place Thames Water (and any other companies failing to meet their statutory duties) into Special Administration due to financial distress and failure to meet licence and performance requirements.

- Submit a plan to the court to cancel the company’s debt, ensuring it is not transferred to the public purse.

- Ensure the Special Administrative process is transparent and time-limited.

- Allow all ownership models to be considered by the Special Administrator, without restriction, until the company’s full state is understood and the public has been consulted. This must mark the end of the current profit-driven model.

- Protect consumers by guaranteeing that public money secures clean rivers, lakes, and seas—not private profits.

Your response fails to directly address the following points, please provide the clarification requested:

Special Administration

We outlined why Thames Water meets the legal threshold for Special Administration under the 1991 Water Industry Act. To reiterate common ground, the law allows the government to take control of water companies either due to financial distress or for breaching statutory duties. Thames Water meets both criteria and the latter condition is clearly met by every water company given the widespread illegality demonstrated by Professor Peter Hammond, triggering Ofwat and EA investigations. Your response simply restates the legal conditions for Special Administration—information we already know. You have not provided any justification for why Thames Water does not meet this threshold.Please clarify why, based on your criteria, Thames does not qualify for Special Administration.

Cancelling Debt and the Costs of Special Administration

We asked the government to submit a plan to the court, as part of the SAR, to discount the debt on the companies.You stated: “The role of the Special Administrator does not include a power to ‘cancel debt’…”

However, you fail to address our core point: the government has the power to apply to the court to cancel the company’s debt as part of the SAR. This would prevent the public from inheriting liabilities caused by private sector failure. You did not explain why the government would not use this power.

Please confirm why you would not apply to the court to cancel the debt.

Transparency and Time-Limiting the Special Administration Process

You have not addressed our request for the Special Administration process to be transparent and time-limited.Please confirm whether you will commit to transparency and a clear timeframe for the SAR.

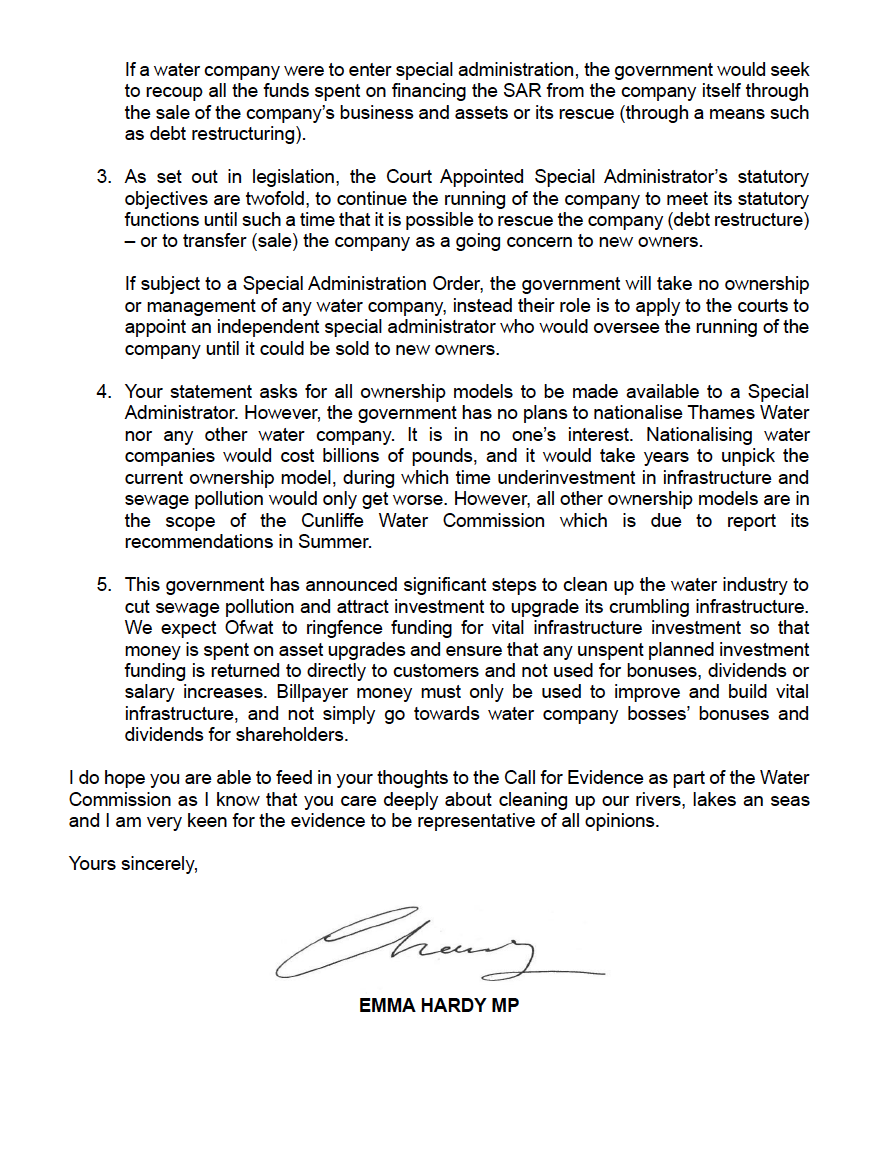

All Ownership Models in Scope

We requested that all ownership models remain on the table. Your response instead argues against nationalisation, stating: “Nationalising water companies would cost billions of pounds…”

You have not provided current, evidence-based analysis to support this claim.

The 2018 Social Market Foundation report you rely on has been discredited due to water company sponsorship. Moody’s, the credit rating agency, estimates nationalisation would cost £14 billion—a fraction of your claim. Moreover, as customer bills have already covered water company costs, but debt repayments now consume a significant portion, continuing with the current model is likely more expensive.

- The current evidence and modelling the government is using to justify its cost claims regarding public ownership.

- Your modelling comparing the long-term cost of public ownership against the continuation of the current privatised model.

- The evidence of private investment in the water industry since 1989, as well evidence of private investment over the next five years.

You state: “Billpayer money must only be used to improve and build vital infrastructure, not for bonuses or shareholder dividends.”

However, this contradicts reality.

At the EFRA Committee, water company CEOs confirmed that customer bills alone could cover all infrastructure costs if it weren’t for the burden of debt repayments. Water companies still plan to pay dividends in PR24, and debt repayments with interest rates over 8% effectively act as a hidden dividend to creditors. Members of this group have written to EFRA setting out the evidence from their committee. Prof Malby will forward this evidence to you.

How will you guarantee that bill payer money is not diverted to dividends or disguised debt payments?